Gen Z Can't Afford a House: What to Know About Lending Within Families

Word count: 1,578 | Read time: 7 min

Buying a first home used to be hard. Now, for millions of Americans in their late 20s and early 30s, it feels closer to impossible. Median home prices have climbed to roughly five times the median household income, according to the Harvard Joint Center for Housing Studies, nearly matching all-time highs, while the median age of a first-time buyer hit 38 in 2024, up from 29 in 1981, per NAR's 2024 Profile of Home Buyers and Sellers. If you have a parent or relative who wants to help you buy (or if you are that parent), an intrafamily loan is one of the most tax-efficient tools available. But the IRS has strict rules, and a handshake agreement between family members is not a loan in the eyes of the tax code. Here is what both parties need to know before a dollar changes hands.

How the IRS Rules Actually Work

Most families skip the paperwork and create an expensive problem without realizing it.

The governing statute is IRC Section 7872, and it establishes a simple but firm rule: if a family member lends money at a rate below the Applicable Federal Rate, the AFR, the IRS treats the forgone interest as a taxable event. Specifically, it deems the lender to have received that interest income (taxable to them) and then gifted it back to the borrower (counted against the lender's annual gift exclusion or lifetime exemption). This happens whether or not any money actually changed hands. The mechanism is called imputed interest, and it applies automatically when the stated rate on the loan falls below the IRS benchmark.

The AFR is published monthly by the IRS and varies by loan term. For June 2026, per IRS Revenue Ruling 2026-11, the short-term AFR (loans up to three years) is 3.85%, the mid-term AFR (three to nine years) is 4.13%, and the long-term AFR (more than nine years) is 4.87%. In an environment where 30-year conventional mortgage rates have hovered well above 6%, these rates represent a meaningful discount: real money saved over the life of a loan. The AFR in effect when the loan is signed locks in for the duration of the loan, so timing matters.

One narrow exception exists: under IRC Section 7872(c)(2), the imputed interest rules do not apply to gift loans where the total outstanding balance never exceeds $10,000, provided the proceeds are not used to purchase income-producing assets. For a home loan of any meaningful size, this exception is irrelevant. There is also a separate provision under IRC Section 7872(d) that limits imputed interest income to the lender when the loan balance falls between $10,001 and $100,000. This is a ceiling on the lender's phantom income, not a blanket exemption from documentation requirements. In both cases, the need for a written loan agreement remains.

The annual gift tax exclusion in 2025 and 2026 is $19,000 per recipient, up from $18,000 in 2024, per Kiplinger and IRS guidance. A married couple who gift-splits can give $38,000 per year to any individual without touching the lifetime exemption, which sits at $15 million per person for 2026 per Morgan Lewis.

The Affordability Gap Is Real

The numbers behind why this generation needs help are not anecdotal.

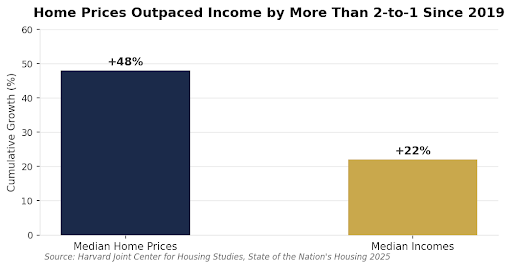

From 2019 to 2024, median home prices rose 48% while median incomes grew only 22%, meaning the gap between earnings and purchase price widened dramatically in just five years.

From 2019 to 2024, median home prices rose 48% while median incomes grew just 22%, according to the Harvard JCHS State of the Nation's Housing 2025. The national price-to-income ratio now sits around 5.5, compared to a historical norm closer to 2.6, per HJFINC's affordability analysis. A household needs an income of roughly $112,000 to afford a median-priced U.S. home, approximately $25,000 more than the national median household income. Meanwhile, NAHB research found that nearly 75% of U.S. households could not afford a median-priced new home in 2025.

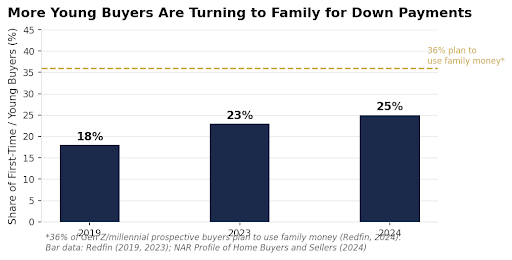

The share of first-time buyers who used family loans or gifts for a down payment rose from 18% in 2019 to 25% in 2024, with 36% of Gen Z and millennial prospective buyers planning to use family money going forward.

The borrowing trend tracks this. In 2019, Redfin found that 18% of young buyers used family money for a down payment. By 2024, the NAR put that number at 25% of first-time buyers. A separate Redfin survey found 36% of Gen Z and millennial prospective buyers plan to use family money for a down payment, making it the second-most-common source after personal savings. The median down payment for first-time buyers in 2024 was 9% of the purchase price, the highest since 1997, and a figure that translates to somewhere near $37,000 on a median-priced home. That is not a small number to accumulate on a $60,000 to $100,000 income while also paying rent.

Building wealth that outlives you starts with getting into the asset. For families who have the means to help, structuring that help as a loan rather than an outright gift can protect both parties: legally, financially, and relationally.

What the Loan Agreement Must Include

A promissory note without these elements is not a promissory note the IRS will respect.

The documentation requirements for an intrafamily loan are not burdensome, but they are non-negotiable. According to Davis Wright Tremaine and Wiggin and Dana, a defensible promissory note must include: the principal amount, a stated interest rate at or above the applicable AFR, the loan term and maturity date, a repayment schedule with actual payment amounts and due dates, default terms, and signatures from both parties. Payments must then actually be made on schedule. A promissory note with no payment history is a document, not a loan.

To unlock the mortgage interest deduction for the borrower, the loan must go one step further: the lender must hold a recorded lien on the property, a mortgage or deed of trust filed under state law. Per IRS Publication 936 and analysis from National Family Mortgage, only secured debt qualifies as home acquisition debt. Without the lien, the borrower cannot deduct interest payments, even if all other requirements are met and the borrower itemizes.

The risks of skipping any of these steps are serious. EisnerAmper's analysis of Bolles v. Commissioner illustrates how the IRS and Tax Court treat intrafamily loans: when documentation is absent, payments are never made, or a prearranged plan to forgive the debt exists from the beginning, the IRS recharacterizes the entire transfer as a gift at the outset, triggering gift tax, back interest, and potential penalties. The intent has to be genuine, and the paper trail has to show it.

Tax Implications for Both Sides

The interest income is real income to the lender. Ignoring that is a costly mistake.

For the lender, interest received on a family loan is ordinary income and must be reported on Schedule B of Form 1040. There is no Form 1098 requirement from a family lender as there would be from a bank, so both parties should maintain careful records of every payment made and received. The annual gift exclusion of $19,000 per recipient ($38,000 for a married couple splitting gifts) can be used each year to forgive a portion of the outstanding balance, if that is the plan. Certuity notes this must be documented as an annual act of forgiveness, not a pre-arranged intent from day one. A lender who plans from the outset to forgive the loan risks having the whole arrangement recharacterized as a gift under MJCPA's analysis of IRS enforcement patterns.

For the borrower, the mortgage interest deduction is available if the loan is secured and recorded and the borrower itemizes deductions, the same requirement that applies to any conventional mortgage. The interest paid to a family member is deductible to exactly the same extent as interest paid to a bank, provided all structural requirements are met.

One more consideration on the lender's side: the outstanding loan balance is part of the lender's taxable estate. If the lender dies while the loan is still active, the balance is included at face value, per the National Association of Estate Planning Councils. The loan does not disappear. It transfers to the lender's heirs or estate unless the will directs otherwise. This is worth discussing with an estate attorney before anyone signs anything.

When a Family Loan Makes Sense

Not every family should do this. Have the money conversation before the legal one.

An intrafamily loan works best when the lender has liquid capital that would otherwise earn less than the AFR. Lending at 4% beats leaving money in a savings account earning 2%, and the interest stays inside the family. Northern Trust and Mercer Advisors both note that the strategy works when both parties can talk about money openly: terms are clear, payments are expected, and the relationship can withstand a financial obligation.

It becomes complicated when the lender needs the capital back for retirement or healthcare, when siblings will perceive the arrangement as inequitable, or when the borrower's income is not stable enough to sustain payments. Mercer Advisors flags that intrafamily loans "can create jealousy and relational problems among siblings," a risk that matters as much as any IRS rule.

If the goal is really a gift (if the parent never truly expects repayment), a cleaner path is using the annual exclusion to gift directly, up to $19,000 per year per parent ($38,000 for a married couple), without the complexity of a promissory note. Down payment assistance programs through state housing agencies and FHA loans (which allow as little as 3.5% down) are also worth exploring before structuring a family lending arrangement. The intrafamily loan is a powerful tool. It is not the only one.

If your family is considering this option, start the conversation well before you are under contract on a home. The IRS rules are specific, the timing matters, and the documentation takes time to get right.

Longitude Financial Planning is a fee-only registered investment adviser dedicated to fiduciary advice for the households we serve. This article is provided for educational purposes and reflects our perspective as of the date of publication; it is not personalized investment, tax, or legal advice. Tax laws, regulations, and market conditions change, and the strategies discussed may not be appropriate for every reader. We encourage you to consult a qualified professional, ideally one held to a fiduciary standard, before acting on any information here.