Estate Planning With Your Parents

Word count: 1,432 | Read time: 6 min

You have organized your own 401(k), sorted out beneficiary designations after the last RSU vesting event, and built a household plan that finally feels like it is working. But estate planning with parents is one of the most deferred conversations most high-earning professionals face, and it has nothing to do with their own finances at all.

At some point in the next decade or two, the question stops being hypothetical. What happens to their home? Who makes medical decisions if they cannot? Does anyone know where their accounts are held? What gets passed down, and how much of it survives probate, family conflict, and years of unchecked assumptions, depends largely on conversations most families have not had yet.

The Documents That Matter

Your parents' wishes are invisible to the law without the right documents.

Five core documents form the foundation of any estate plan: a will, a durable power of attorney, a healthcare proxy, current beneficiary designations, and for many families a revocable living trust. Each one does something different, and the absence of any single one creates a different kind of problem.

A will directs how property is distributed at death, names an executor to carry out those wishes, and designates a guardian for any minor grandchildren. Without one, the state's intestacy laws take over, as NOLO explains, and those laws carry no information about family dynamics, recent estrangements, or promises made around a kitchen table.

A durable power of attorney names an agent to manage financial affairs if your parent becomes incapacitated. The word "durable" is not incidental: a standard power of attorney terminates the moment the principal loses capacity, per NOLO, which is exactly when legal authority to help is most needed.

A healthcare proxy designates who makes medical decisions when a parent cannot speak for themselves. An advance directive records their end-of-life care preferences in writing. Many states combine both into a single form, according to the National Institute on Aging, which also offers free worksheets families can complete together.

Beneficiary designations may be the piece most commonly misunderstood. Whatever a will says, it does not control what happens to a 401(k), an IRA, a life insurance policy, or a payable-on-death bank account. Those assets transfer directly to whoever is named on file, outside of probate entirely, as Policygenius explains. A designation set in 1998 and never revisited is, legally speaking, the current plan.

For families with real estate in multiple states or a preference for privacy, a revocable living trust can hold assets and distribute them at death without court involvement. The Consumer Financial Protection Bureau notes that a revocable trust does not reduce estate taxes on its own; it is a distribution and privacy tool. What it avoids is significant: probate typically costs 3% to 10% of the gross estate value and can take anywhere from six months to two years to resolve, per Policygenius.

How to Start the Talk

Most people know this conversation needs to happen. Very few know how to start it.

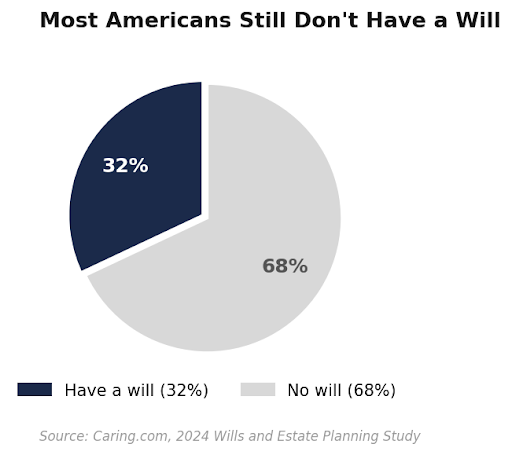

According to Caring.com's 2024 Wills and Estate Planning Study, only 32% of Americans currently have a will, a figure that dropped six points from the prior year. More than half of American adults believe people should have a will by age 35. The average age they actually create one is 42. The gap between knowing and doing is not a knowledge problem.

Despite widespread awareness that estate planning matters, fewer than one in three Americans has a will as of 2024.

Financial planning for elderly parents also carries a specific emotional weight that other money conversations do not. Forty-three percent of adults without a will cite procrastination as the reason, and another 40% say they do not have enough assets, per Caring.com. That second number reflects a persistent misconception: estate planning is not only about who inherits money. It is about who holds legal authority and whose wishes are documented when decisions cannot wait.

Starting with values rather than logistics tends to work better in practice. "What is most important to you about how things are handled if something happens?" is a more useful opening than "do you have a will?" It signals care for their choices rather than anxiety about outcomes. If no natural moment presents itself, a parallel framing helps: you have been doing your own financial planning for parents and want to make sure your family is on the same page.

Triggering events open the door on their own. A parent's retirement, a friend's complicated estate, a new grandchild, or a health scare all create on-ramps that feel less like an intervention and more like a logical next step. Multiple conversations over time accomplish more than a single comprehensive session, and a private, unhurried setting matters more than the right script.

When Senior Generations Push Back

Procrastination is the most common reason families skip this conversation. A crisis is a terrible time to start it.

When a parent resists, the most useful reframe is also the most accurate one: estate planning is about control, not death. A durable power of attorney and healthcare proxy let your parents decide in advance who acts on their behalf, rather than leaving that choice to state law or a court. The premise is autonomy, not surrender.

Family conflict in the absence of documentation is not rare. According to Lesser Lutrey Pasquesi & Howe, 44% of estate disputes involve siblings, and 30% of families involved in inheritance conflicts stop speaking to each other entirely. These outcomes are not caused by bad intentions. They are caused by assumptions, gaps in documentation, and the absence of a named decision-maker.

If parents remain reluctant after one conversation, plant the seed and return to it in a few months. The goal is not resolution in a single sitting but an open door that stays open.

Bring In a Professional

One meeting with the right team can accomplish what years of gentle hints at dinner cannot.

Two professionals tend to collaborate in this process, each with a distinct role. An estate planning attorney drafts and executes the legal documents: the will, the trust, the durable power of attorney, and the advance directive. As NerdWallet explains, these documents must conform to state law, which varies considerably, and a generic online template often falls short.

A fee-only fiduciary financial planner coordinates the financial picture alongside the legal structure. NAPFA defines fee-only as compensation drawn exclusively from client fees, with no product commissions. Fiduciary means the advisor is legally required to act in the client's interest. These terms are related but not interchangeable, as Kiplinger notes: a fee-based advisor may earn commissions on some products while still holding fiduciary status on certain advice.

For parents who are skeptical, framing the first meeting as a discovery conversation rather than a commitment lowers the barrier considerably. They are not signing anything. They are learning what they have and whether any gaps need attention.

Building Wealth That Outlives You

What your parents built over a lifetime deserves a plan worthy of it.

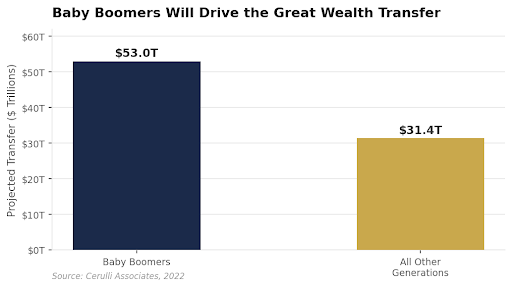

Baby Boomers account for more than 63% of all projected generational wealth transfers through 2045, making estate planning with parents one of the defining financial conversations of the coming two decades.

The scale is significant. Cerulli Associates projects $84.4 trillion in wealth will change hands through 2045, with $72.6 trillion going to heirs and $11.9 trillion to charitable causes. What happens to those assets depends on decisions families make long before any of it transfers.

One concept that surprises many families is the step-up in basis. Under IRC Section 1014, assets inherited at death receive a new cost basis equal to their fair market value on the date of death, eliminating the capital gains tax on appreciation that accumulated during the owner's lifetime. A parent who bought stock at $10 per share and held it to $100 per share has an embedded $90-per-share gain. An heir who inherits those shares pays no tax on that appreciation. The same rule does not apply to inherited IRAs or 401(k)s, which carry ordinary income tax on distributions regardless of how they are received.

Most families will not owe federal estate taxes. The exemption for 2026 is $15 million per individual, or $30 million per married couple, per ElderLawAnswers, which means the more common threats to a family's estate are probate costs, family conflict, and a mismatch between what parents intended and what the law defaults to in the absence of documentation.

Loving couples make it easier for each other. That instinct extends across generations. When your parents document their wishes, name their agents, and coordinate their accounts with a clear structure, they are not only preserving assets. They are protecting relationships, including yours. Building wealth that outlives you starts with making sure those decisions are written down.

If you are thinking about estate planning for your parents, or your own, it helps to have a team that can coordinate both sides. We work with families at exactly this stage of life, helping you ask the right questions and making sure the documents, accounts, and plan are pointing in the same direction. This is one of the most meaningful steps you can take, for your parents and for the people who come after you.

Longitude Financial Planning is a fee-only registered investment adviser dedicated to fiduciary advice for the households we serve. This article is provided for educational purposes and reflects our perspective as of the date of publication; it is not personalized investment, tax, or legal advice. Tax laws, regulations, and market conditions change, and the strategies discussed may not be appropriate for every reader. We encourage you to consult a qualified professional, ideally one held to a fiduciary standard, before acting on any information here.