How Private Equity Powers the Data Center Boom (And Why it Belongs in Your Portfolio)

Word count: 1,496 | Read time: 6 min

If you live in a high-cost metro, earn well as a couple, and still feel like your money is scattered across accounts that do not talk to each other, you are not alone. Plenty of households earning more than $150K combined still feel behind, and one reason is that the most interesting parts of the modern economy stay locked behind doors most investors never see. The buildout powering artificial intelligence is the clearest example. You can read about it every day, you can watch the headlines, and you can still have almost no real ownership of it. Private equity is the vehicle that changes that, and data centers are where the case is strongest right now.

The Three-Reason Case

The most valuable assets in the AI economy are not the ones you can buy in a brokerage account. They are the buildings underneath it.

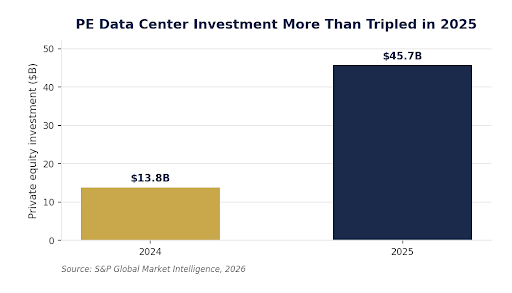

Private equity poured a record amount into U.S. data centers in 2025, more than tripling the prior year's total.

The first reason is durable, contracted cash flow. A hyperscale data center is not leased the way an apartment is. The big cloud tenants sign single-tenant leases that run 10 to 15 years, often with built-in rent escalators, while smaller colocation deals run 5 to 7 years (CBRE Investment Management).

Roughly 90% of hyperscale facilities are pre-leased on 10-year-plus contracts before construction even starts (Columbia Business School). The tenants signing those leases are among the most creditworthy companies on earth: Amazon carries an AA rating, Microsoft AAA, and Google AA, and the top five tenants account for about 73% of all leasing (CREFC). That is rent you can underwrite with real confidence.

The second reason is inflation resistance. Data centers behave like infrastructure, a category of real assets that has held up when prices rise. Many leases pass operating costs straight through to the tenant and index rent to inflation, so the income stream tends to climb alongside the cost of living (KKR).

A 50-year backtest from PGIM found that adding real assets to a stock and bond mix produced positive active returns of roughly 5.6% to 10.9% over a standard 60/40 portfolio during high and rising inflation (PGIM).

For a couple thinking in decades, that durability matters more than any single year's headline return.

The third reason is access. The capital is moving fast, and most of it is private. Private equity invested $45.70 billion in U.S. data centers in 2025, about 72% of all capital that flowed into the sector and the highest figure in at least five years (S&P Global Market Intelligence).

Blackstone alone disclosed a global data center portfolio worth more than $150 billion, plus another $160 billion in pipeline, on its 2026 first-quarter earnings call (Bisnow). The single largest investors in the AI buildout are private funds, not public shareholders, and that is the gap private equity lets an accredited household close.

Public Stocks Versus Private

You can buy a piece of this story on any screen. Owning the engine of it is a different transaction entirely.

There is a real public market here, and it deserves credit. If you want data center stocks today, you can buy listed REITs like Equinix or Digital Realty in any brokerage account or IRA, with full liquidity and no minimum (Nareit).

For many dual income investors, those names are a sensible first step and an easy way to get exposure. When someone asks me which data center stocks to buy, the honest answer is that public REITs give you a liquid, diversified slice without locking up a dollar.

What they do not give you is the development upside or the illiquidity premium that lives in private deals. The temptation some people have is to go further and look for a data center for sale directly, as if it were a rental property. That path is a dead end for an individual. A single hyperscale facility costs hundreds of millions to billions to build, runs on specialized power infrastructure, and can wait years in a grid connection queue. Private equity and infrastructure funds exist precisely to pool capital so that ownership becomes possible at all.

Getting in requires meeting the accredited investor standard. The SEC defines that as income above $200,000 individually, or $300,000 jointly with a spouse, in each of the last two years, or a net worth above $1 million excluding your primary residence (SEC).

Larger private funds add a higher bar, the qualified purchaser standard, which generally means holding $5 million or more in investments (SEC).

Many of these offerings are sold under Regulation D Rule 506(c), which lets sponsors advertise but requires them to verify your status with tax forms or a letter from your CPA or adviser (SEC).

The threshold is a real gate, and for a strong-earning couple it is often closer than you would guess.

The Risks Behind The Returns

Every dollar of contracted rent depends on one quiet assumption. The power shows up on time.

The same demand that makes these assets attractive is colliding with a power grid that was not built for it.

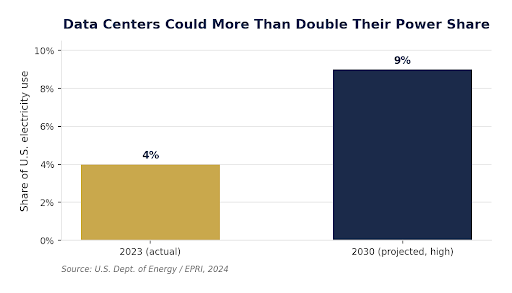

The biggest near-term risk is electricity. U.S. data centers used about 4% of the nation's power in 2023, and projections show that climbing toward 9% by 2030 (U.S. Department of Energy).

Getting that power to the right place is the hard part. Some grid connection requests now face waits of up to seven years, and 72% of industry executives call power and grid capacity very or extremely challenging (Deloitte). S&P Global flags this mismatch directly, noting that delays mean "the chips not getting turned on at the right time, which leads to revenue not coming in the door on schedule" (S&P Global Market Intelligence).

Liquidity is the second honest tradeoff. Private funds typically lock capital for 7 to 12 years and call it in over time, which produces the J-curve: returns dip early as fees accrue before investments mature, then climb. Buyout funds historically took about four years to reach the bottom of that curve and seven to turn cash-flow positive, though infrastructure funds tend to have a flatter ride (Apollo Academy). You also carry concentration risk, since a handful of hyperscalers anchor most leases, and demand risk, since the whole thesis rests on AI staying profitable enough to justify the buildout (S&P Global Ratings).

Fitting It To Your Plan

A great asset in the wrong size is still a mistake. The allocation question matters more than the headline.

This is where the decision stops being about data centers and starts being about your household. Institutions now routinely hold 20% to 30% of their portfolios in alternatives, and Morgan Stanley's investment committee suggests alternatives can make up as much as 25% of an efficient portfolio, with KKR recommending a minimum 5% allocation to private infrastructure (Morgan Stanley).

The reason they accept the lock-up is the illiquidity premium: private infrastructure returned 9.9% annualized over the past decade against 6.5% for the public index (Pantheon).

The catch is that a capital call does not care about your timing. If you commit to a fund, you need cash ready when the manager draws it, even if a tuition bill or a home purchase lands the same quarter. These funds also generate K-1 tax forms and long holding periods that ripple into your tax return and your estate plan. None of that is a reason to avoid the asset. It is a reason to size it deliberately, inside a written plan that already accounts for your equity compensation, your property, and your liquidity needs. Loving couples make this easier for each other when they decide together how much risk and how much lock-up the household can carry, rather than reacting to a pitch one of them heard.

The data center boom is real, and private equity is the most direct way for qualified households to own it. The work is matching the opportunity to your actual balance sheet.

If you are weighing whether data center stocks, a private infrastructure fund, or some mix of both belongs in your portfolio, that decision should sit inside your broader plan, not on the side of it. Our financial planning practice in Austin, Texas works with dual income couples to size alternatives sensibly, coordinate the tax consequences, and keep enough liquidity for the life you are actually building. Bring your questions and we will map a clear, unhurried path together.

Longitude Financial Planning is a fee-only registered investment adviser dedicated to fiduciary advice for the households we serve. This article is provided for educational purposes and reflects our perspective as of the date of publication; it is not personalized investment, tax, or legal advice. Tax laws, regulations, and market conditions change, and the strategies discussed may not be appropriate for every reader. We encourage you to consult a qualified professional, ideally one held to a fiduciary standard, before acting on any information here.